From Healthcare Affordability Crisis to Transformation, Now.

February 17, 2026

The healthcare affordability crisis is not a moment to pause. It’s the moment for health plans to transform.

The healthcare affordability crisis might be pushing health plans to pull back—to retrench, regroup, and wait for calmer waters. It is an understandable instinct, but one that comes with distinct risks.

Transformation is no longer optional. The affordability crisis is forcing every health plan to confront cost, quality, and value in ways that they could previously defer. While the worsening affordability crisis is a headwind, it is also a catalyst for innovation and competitive differentiation, but the time to act is now.

At NASCO, our perspective on the affordability crisis is shaped by 40 years in healthcare. We began in 1987 supporting national accounts and have evolved alongside the industry. Today, our products and services support health plans across nearly every line of business, at scale.

The NASCO evolution matters. Over four decades, we have learned that standing still is one of the fastest ways to fall behind. Just as NASCO has expanded and adapted to meet the changing needs of payers, the role of the health plan too must evolve.

At a time when healthcare feels more complicated than ever, the role that the health plan plays is more critical than ever. Providing access to affordable care requires holistically marrying clinical innovation and access with product packaging and benefit designs to incent members to the right care, at the right place, in the right time—all wrapped in an experience to help navigate complexity.

This is the first in a series of blogs from NASCO leaders focused on one question: how health plans can move decisively and embrace the transformation imperative.

The healthcare affordability crisis has reached a tipping point.

Let me first affirm that we at NASCO know the pain of the healthcare affordability crisis is acute, real, and impacts all stakeholders—members, employers, providers, and health plans.

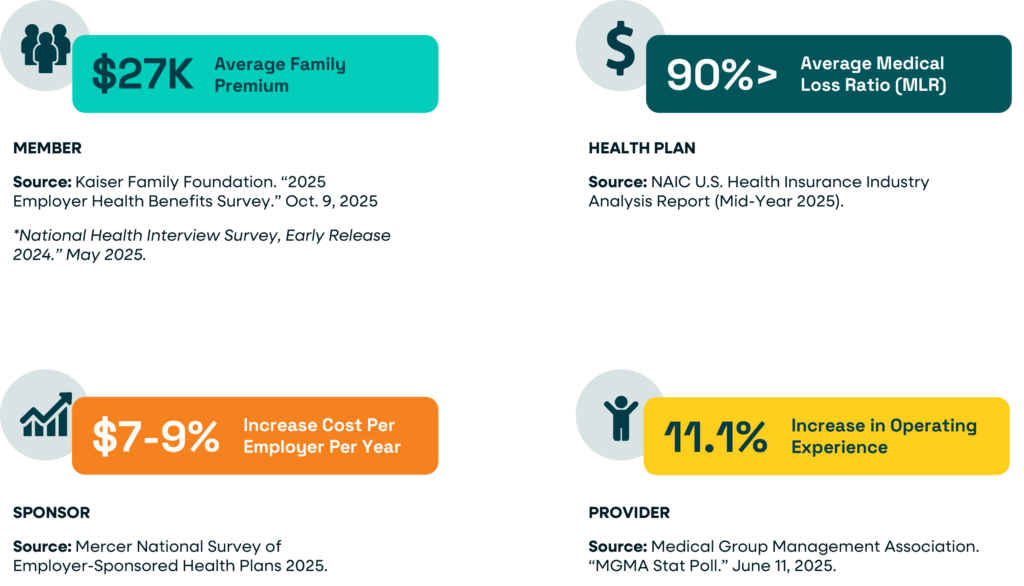

- $27K, Average family premium

- 66%, Americans very or somewhat worried about paying for healthcare

- 7-9%, Increase in cost per employer per year.

- >90%, Average payer medical loss ratio (MLR)

- 11.1%, Rise in provider operating expense

- 7.2%, Growth in total U.S. healthcare spending to $5.3 trillion in 2024, largely driven by utilization and more complex services, not price increases

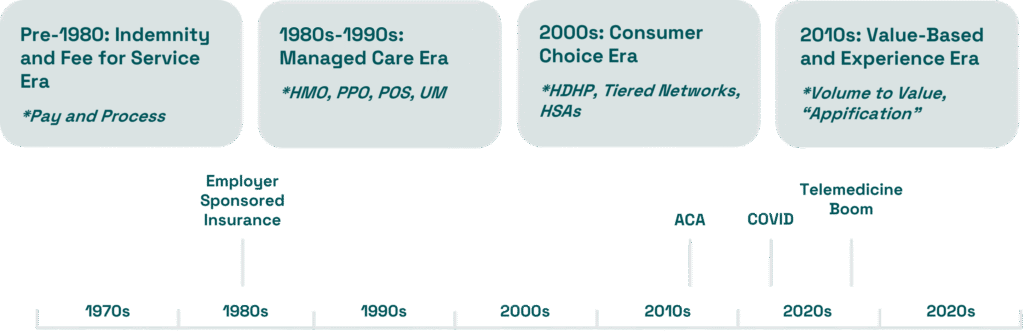

Healthcare Affordability Approaches: The Evolution of Cost Containment Levers

The cost containment approaches employed to drive healthcare affordability have evolved.

I have spent more than 30 years with a front-row seat for healthcare’s cost-containment initiatives. My career began in behavioral practice management and has spanned both sides of the system—inside regional and national health plans, and building solutions across health tech, consumerism, and direct primary care, including a 65-practice model serving employers directly.

In other words, I have lived the approaches to healthcare affordability, from within the system, and I know important lessons were learned.

Healthcare Affordability Approaches: The 1980s-1990s Managed Care Era

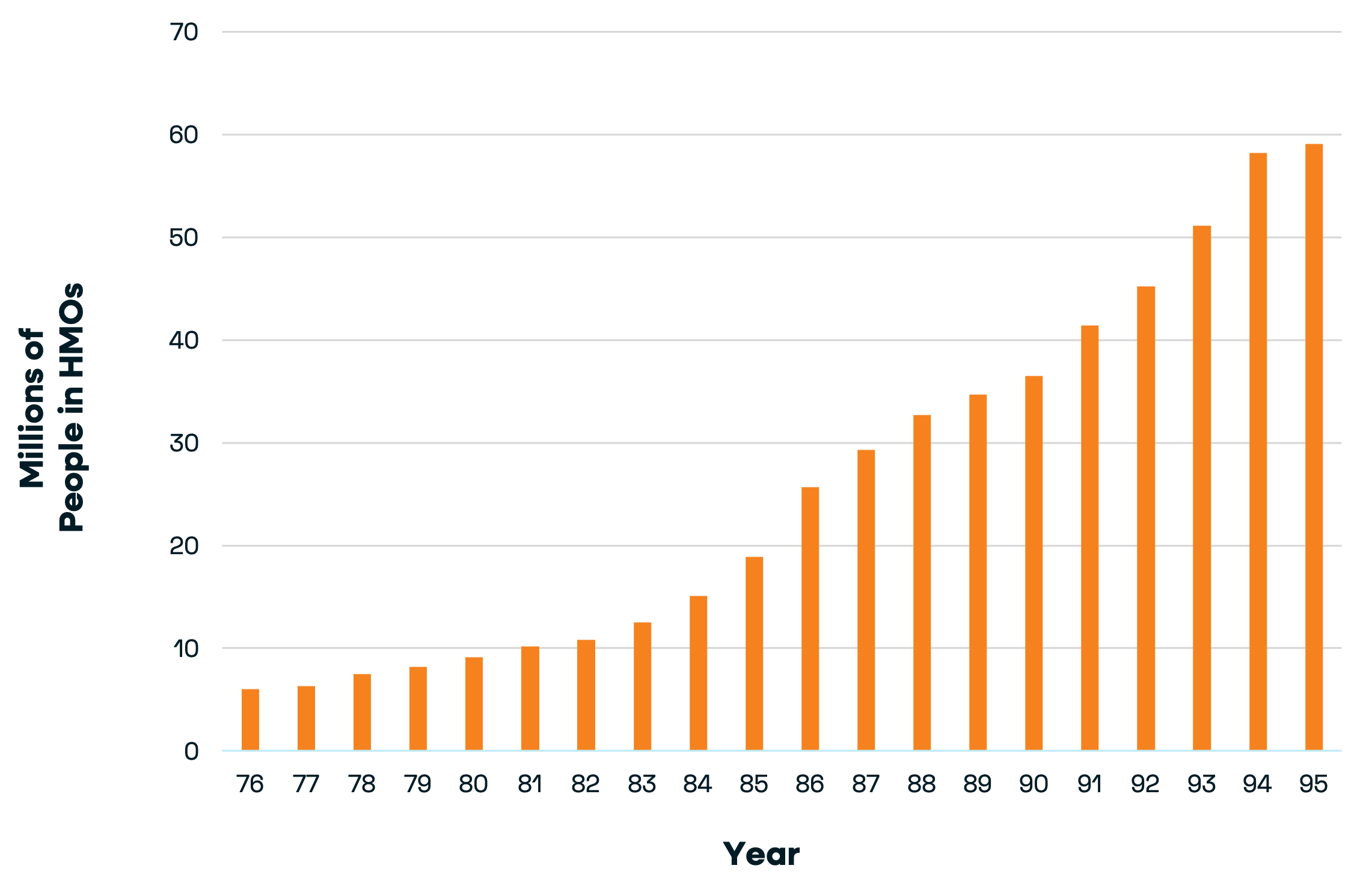

Remember HMOs? By 1996, more than half of the U.S. population and nearly three-quarters of insured employees were enrolled in 600+ health maintenance organizations (HMOs), a preferred provider organization (PPO) or another type of managed care organization.

HMO Enrollment, All Ages, 1976-1996

Starting in the 1980s and 1990s, health plans adopted managed care, utilization management, narrow provider networks, capitation, and fixed payments. The primary care physician (PCP) became the gatekeeper.

Historical reviews show HMOs became highly effective at measuring and controlling costs, but paid too little attention to health outcomes, resulting in consequences on the member/patient side and ultimately triggering backlash. The savings were fragile and hospital spending rose again, more than doubling from $168 billion in 1985 to roughly $360 billion by 1996.

Healthcare Affordability Approaches: The 2000s Consumer Choice Era

In the 2000s, the industry moved from provider-led to consumer-directed care. At the time, I worked for a consumer choice startup that empowered members to configure plan design to address their personal needs. For example, a lower cost share for pediatric visits and a higher copayment for hospitalizations. The enduring innovation from that time was the high-deductible health plan, enabled by levers with our core systems.

A defining hallmark of the consumer choice era was an emphasis on individual, choice, transparency, and market competition. At the time, the industry assumed that patients, equipped with price and quality information, would shop for care, and well-informed patients would drive high-value purchasing as the result of spending more of their own money—assumptions that would ultimately prove untrue.

The industry created a number of tools and offerings during the consumer choice era including:

- High-deductible health plans (HDHPs),

- Health savings accounts (HSAs),

- Price transparency tools,

- Shopping platforms and quality scorecards, and

- Incentives for ‘value shopping.’

The laudable goal was to empower consumers; however, the care team was not included, leaving members without care navigation resources. Even more importantly, the tools of the consumer choice era assumed patients would behave like rational shoppers, but this quickly eroded during illness, e.g., a mother takes her inconsolable toddler to the ER, or when complexity was high. Despite marginal advances in providing price and quality data, the consumer choice era had a limited impact on overall costs.

Healthcare Affordability Approaches: The 2010s Value-Based Care and Experience Era

Enter value-based care (VBC) and the right care, at the right time, at the right place. The Triple Aim—improving population health, patient experience, and the per capita cost of healthcare—becomes foundational to value-based care. The Quadruple Aim expands upon this by adding a fourth essential goal: improving the work life and well-being of healthcare providers, also known as the Joy of Medicine.

Defining characteristics of VBC are:

- The focus is on outcomes, quality, equity, and total cost of care, not the amount of services delivered.

- Providers are rewarded for keeping patients healthy, improving population outcomes, and preventing avoidable utilization.

- Payment is tied to results, not volume.

Unlike previous eras, the VBC era correctly focused not only on who pays and how much, but also the cost of care. Where this fell short was in attempting to shift the healthcare system before we had the purposeful infrastructure required for success at scale.

Healthcare Affordability Approaches: The Dawn of the Structural Affordability Era

Today, we know narrow, fragmented, and disconnected approaches to healthcare affordability do not impact the total administrative and medical cost equation. The hard-earned lessons from decades of cost-containment efforts are clear: affordability is achievable when medical economics, administrative costs and quality are addressed together—and when the model addresses friction between stakeholders and scales for everyone involved.

Health plans will solve affordability by pulling the structural levers, the ones that move both medical and administrative costs and move them now. Providers must be meaningfully empowered and properly incentivized. Members must be guided as they navigate their care. Progress only happens when the entire ecosystem advances together.

It’s the dawn of the structural affordability era.

Next up in the NASCO series about health plan transformation is Lori Logan’s blog about why traditional approaches to healthcare affordability won’t work. Want to be the first to know when it’s published? Subscribe to the series now.

KFF. 2025 Employer Health Benefits Survey, October 22, 2025

https://www.kff.org/health-costs/2025-employer-health-benefits-survey/

KFF. Americans’ Challenges with Health Care Costs, January 29, 2026

https://www.kff.org/health-costs/americans-challenges-with-health-care-costs/

Mercer. National Survey of Employer-Sponsored Health Plans

NAIC. U.S. Health Insurance Industry Analysis Report, 2025 Mid-Year Results

Medical Group Management Association. Medical practice operating costs are still rising in 2025 — here’s how to control them, June 11, 2025

CMS: US’ total healthcare spending rose 7.2% to $5.3T in 2024 amid high utilization, coverage

https://www.fiercehealthcare.com/finance/cms-us-total-healthcare-spending-rose-72-53t-2024