Healthcare Affordability: Traditional Approaches Are Failing

March 24, 2026

Lori Logan, NASCO President and CEO

Nearly every week, there’s new data showing we have reached the tipping point of the healthcare affordability crisis.

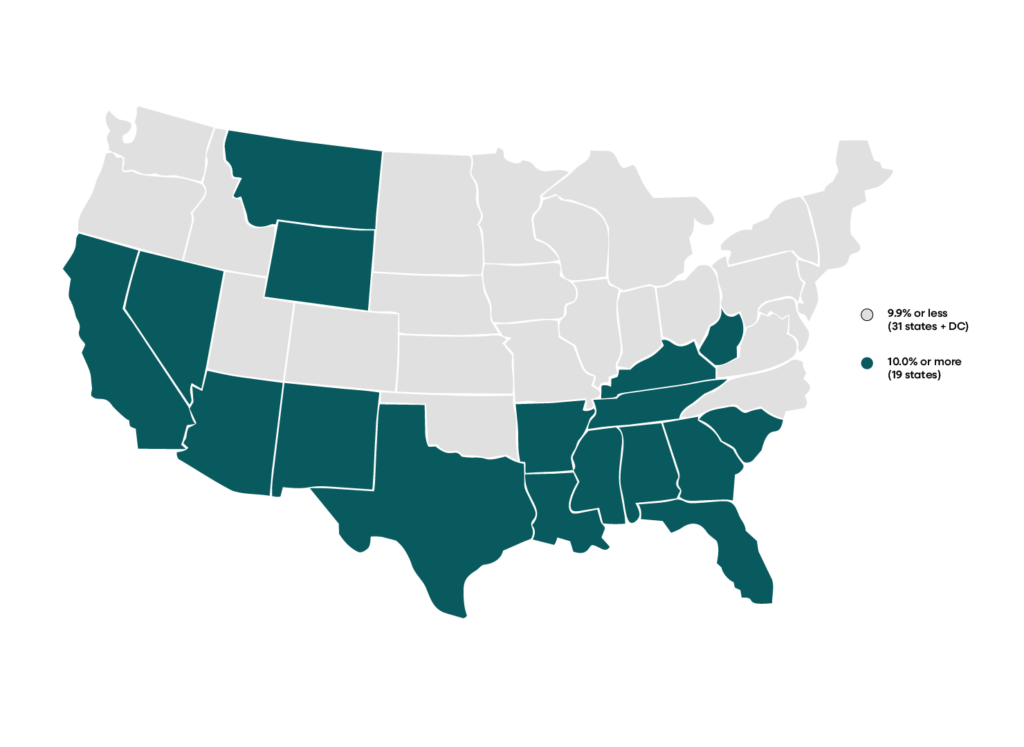

Case in point, a recent Commonwealth Fund study of 2024 data showed the combined cost of health insurance premium contributions and deductibles for family plans totaled 10 percent or more of median family household income in 19 states, an average of 10.1 percent nationally. And that figure does not include copayments and other health insurance costs. In 2001, the median financial burden was 7.3 percent of income, increasing to 8.9 percent in 2009.

Average annual combined premium contributions and deductibles for family premiums as a share of median family income (%) by state.

The average American family spends more than 10 percent of their income on health insurance premium contributions and deductibles.

Kristen Kolb, David C Radley, and Sara R Collins | Source

The President and CEO of Ascendiun, the parent company of Blue Shield of California, Paul Markovich, offered this blunt assessment,

“We think [the healthcare system is] dysfunctional and broken and bankrupting us, and we need structural, systemic change.”

Markovich went on to explain:

“We have to get into a different mindset: How do we make healthcare affordable? We all have to be financially viable, but how do we make healthcare affordable and worthy of our family and friends? That means we have a cost problem that we need to address. I’m hopeful that creating that kind of budgetary, top-down pressure helps create that mindset and gets us into a much more innovative phase in healthcare, one where we really are focused on how to make things better for the patient and more efficiently.”

Paul Markovich, President and CEO of Ascendiun | Source

That’s precisely why NASCO is calling on health plans to embrace transformation and move decidedly into the structural affordability era. For health plans, solving the healthcare affordability crisis requires immediate structural changes that lower both medical and administrative costs and, because real progress will only happen when the entire system moves forward together, robust collaboration with providers and personalized navigation for members. Providers need the right tools and incentives to deliver value and members need clear guidance to enable them to become stewards of their health and care.

Put differently, the role of the health plan is more important than ever in driving affordability, but operationalizing affordability cannot be done in silos. It requires a holistic approach that addresses medical and administrative costs, quality, access, and experience simultaneously.

Why Traditional Approaches to the Healthcare Affordability Crisis Won’t Work

As one who has lived the prior approaches to affordability during my three decades working in healthcare, I understand the temptation to deploy the traditional approaches to cost containment. Afterall, health plans have always competed on cost, quality, and access. Historically, payers have confronted the affordability challenge by focusing on one or two areas, say cost at the expense of access as they did in the Managed Care Era of the 1980s and 1990s or changing who pays or the percentage paid by the employer or consumer.

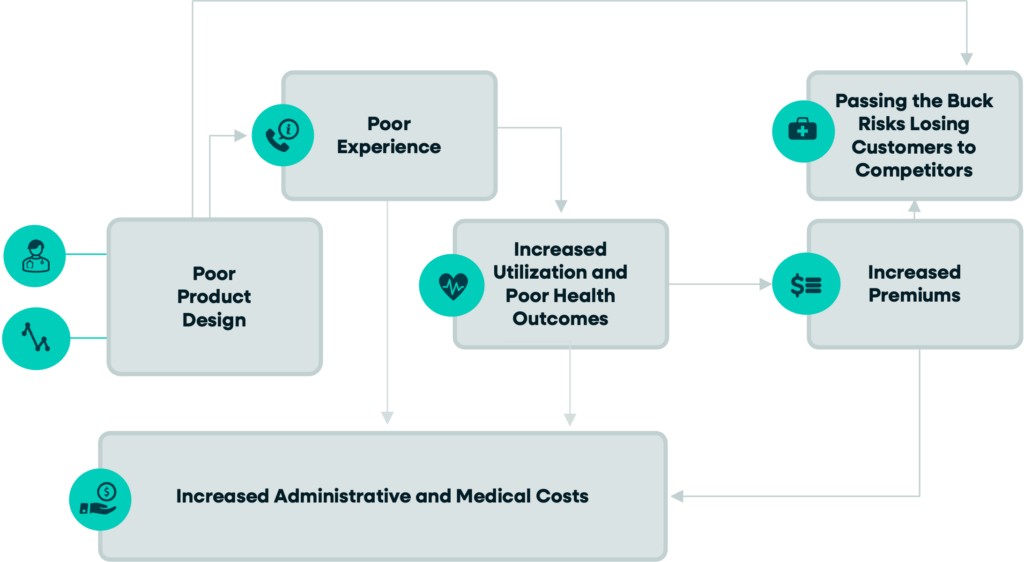

This visual illustrates why incremental, siloed fixes are insufficient to address healthcare affordability—and why a structural shift is required.

Why Traditional Approaches Won’t Cut It

Break the cycle.

Health plans must go beyond siloed approaches and focus on structural leverage points to deliver affordability, now.

When products are built without deep alignment to outcomes, they often lead to poor product design, which creates a fragmented and frustrating member experience. Members struggle to navigate care, delay treatment, or try to access care in the wrong settings. These breakdowns drive increased utilization and poorer health outcomes. As health issues become more acute and less coordinated, both the frequency and intensity of services rise. The result is a compounding effect: administrative complexity and medical costs increase simultaneously.

Historically, the system has responded by attempting to offset these rising costs rather than correcting their root causes. That often means shifting risk to customers through higher premiums or cost sharing, which may stabilize finances in the short term but does nothing to resolve the underlying inefficiencies. In fact, it can restart the cycle—making care less accessible, outcomes worse, and costs even higher over time.

Healthcare Affordability Crisis: Now What?

The message is clear: we will not achieve affordability through isolated optimizations or by simply redistributing costs. It requires pulling the structural levers—aligning product design, provider incentives, member engagement, and operational models—so the entire ecosystem works together to improve outcomes while reducing total cost of care. Only when these elements move in coordination—and it works for all stakeholders—will we break the cycle and replace it with one that consistently delivers value instead of perpetuating cost escalation.

Next up in the NASCO series about health plan transformation is Lori Logan’s blog about how the role of the health plan must evolve to drive affordability. Want to be the first to know when it’s published? Subscribe to the series now.

To read the first blog in the series, From Healthcare Affordability Crisis to Transformation, Now, click here.